News

Canada’s Credit System Shapes Access to Loans, Housing, and Financial Services

In Canada, credit scores play a central role in determining access to financial products, influencing everything from loans and mortgages to rental applications. Lenders and service providers rely on credit reports compiled by major bureaus to assess how individuals manage debt and repayment.

Rather than being used only for large financial decisions, credit scores are applied broadly across everyday situations, including mobile contracts, insurance, and utilities. The system is based on factors such as payment history, credit usage, and overall debt levels, making consistent financial behaviour essential for maintaining access to opportunities and favourable terms.

Rise of Non-Bank Financial Players Is Shifting Systemic Risks Rather Than Eliminating Them, Bank of Canada Warns

The Bank of Canada highlights that the financial system is undergoing structural change, with non-bank institutions such as hedge funds and private credit providers playing a growing role in market activity. While this shift has expanded access to financing, it has also introduced new forms of risk that are less visible than those in traditional banking.

Key concerns include leveraged trading in government bond markets and the rapid growth of private credit, both of which can amplify stress during periods of market volatility. These activities often rely on short-term funding structures, making them more vulnerable to sudden liquidity shocks.

Strong Credit Scores No Longer Shield Homeowners From Mortgage Stress, Equifax Data Shows

Financial strain among Canadian homeowners is no longer limited to traditionally high-risk borrowers, as rising interest rates and cost-of-living pressures begin to affect a wider segment of the population. Recent data from Equifax shows that mortgage delinquencies are increasing across credit tiers, including among borrowers with strong credit histories who would typically be considered financially stable.

The trend points to a broader systemic pressure rather than isolated financial mismanagement, raising concerns about how sustained high rates and affordability challenges could continue to impact the housing market and overall financial stability in Canada.

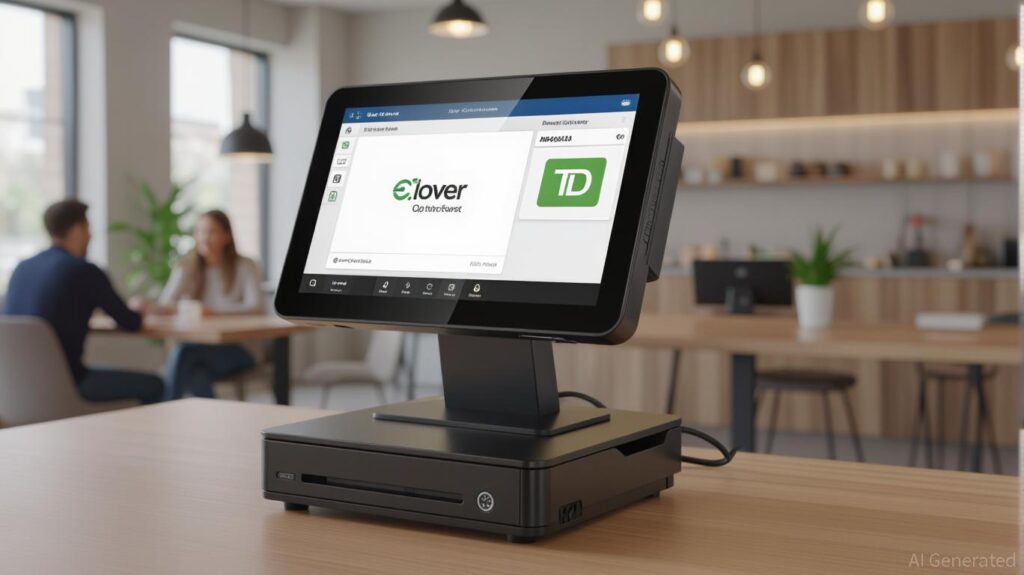

TD’s Strategic Partnership with Fiserv: A Digital Transformation Play with Minimal Disruption

Clover’s full-stack solutions enhance SMB offerings with integrated payments, inventory, and financial tools, differentiating TD in a competitive fintech market

While short-term financial impact is muted, the partnership strengthens TD’s long-term digital resilience and cross-selling potential with clients.

The Toronto-Dominion Bank (TD) has long been a leader in Canadian banking, but in an era where digital transformation is no longer optional, its recent partnership represents a calculated move to future-proof its competitive edge. By integrating Fiserv’s platform into its Merchant Solutions (TDMS) business and divesting a portion of its merchant processing operations, TD is not only streamlining costs but also positioning itself as a more agile player in the rapidly evolving fintech landscape. For investors, the question is whether this strategic shift will translate into sustainable shareholder value.

Exclusive: RBC, BMO planning sale of $2-billion Canadian payments venture, sources say

Aug 14 (Reuters) – Royal Bank of Canada (RY.TO), opens new tab and Bank of Montreal (BMO.TO), opens new tab have placed their Canadian payments joint venture up for sale, in a deal that may value the business as highly as $2 billion, four people familiar with the matter said. Moneris is one of the largest payment processors in Canada, handling one in every three business transactions in the country. It was founded in 2000 by the two banks, and offers digital, mobile, and in-store payment systems for about 325,000 merchant locations, according to its website.

Canada’s fintechs are surging—against all odds

Canadian fintech has been rebounding since 2024. Investment reached a record US$9.5 billion last year, up from US$1.1 billion the previous year, according to data from PitchBook compiled by KPMG. Fintech funding in the country outperformed the sector globally last year, which saw investment drop, and also surpassed other tech sectors in Canada that continue to have difficulty raising funds, such as cleantech.

In January, Float announced a $70-million Series B led by Goldman Sachs’s growth equity arm. The round pushed Float’s valuation about 30 per cent higher than the US$150 million it was valued at following a US$30 million Series A led by Tiger Global in 2021. Fellow Toronto-based fintechs Venn and Loop, as well as Wealthsimple and Koho, have also announced significant fundraises in recent months.

Springtime for Canada’s fintech industry?

The uptake of digital financial services is low in Canada compared with other similar economies. Developments in five areas will determine if the industry is about to blossom

First, its banking industry is large compared with other G-7 countries. Banking revenues of $180 billion accounted for 7.9 percent of GDP in 2023, compared with 5.8 percent in the United States and an average of 5.6 percent among other developed economies. Canadian banks are also more profitable than those in other developed economies (Exhibit 1). Likewise, Canada’s insurance revenue pool is large. With estimated revenues of $136 billion in 2022, it’s one of the world’s ten largest insurance markets.1 These attributes make Canada a tempting target for fintech attackers.

Latest inflation numbers slam door ‘shut’ on Bank of Canada July rate cut, say economists

Rising inflation in June is solidifying economists’ calls that the Bank of Canada will stay on the sidelines at its next interest rate meeting on July 30 and increases doubt about a possible cut at its September meeting.

Article content

The consumer price index (CPI) rose 1.9 per cent in June, according to Statistics Canada on Tuesday, which matched analysts’ estimates, but that’s up from a 1.7 per cent increase in May.

The best fixed and variable mortgage rates this week

Will there be any more interest rate cuts from the Bank of Canada this year? At least one major Canadian bank thinks the answer is no.

A Royal Bank of Canada report last month from RBC Economics says it’s now forecasting no further cutting from the central bank in light of inflation concerns and the Canadian economy’s resilience during the U.S. trade war. It’s bad news for variable mortgage holders who may have been banking on some discounts this year.

Not all economists agree with RBC, with other institutions such as Bank of Montreal forecasting as many as three rate cuts in 2025. But Robert Kavcic, senior economist at BMO Economics, has also said that a trade deal between Canada and the U.S. that puts a stop to tariffs could indeed prompt the Bank of Canada to hold rates for the rest of the year.

The U.S. and Canadian governments have given themselves a July 21 deadline to reach a trade deal, and talks have been rocky along the way. Until we know more about the nature of a possible deal, there is a lot of uncertainty in the direction of variable mortgage rates.

Canadian financial system stable, but trade war poses big risks, says central bank

A prolonged trade war could increase the risks to Canadian financial stability by hurting banks and other institutions and making it harder for households and businesses to pay down debt, the Bank of Canada said on Thursday.

In its annual Financial Stability Report, the central bank said the financial system was resilient.

But the impacts of tariffs slapped by U.S. President Donald Trump on Canada and Ottawa’s subsequent counter-tariffs could hurt financial stability, especially if it continues for a long period of time.

Preparing for the downside: Could Canadian federal finances withstand a trade war?

Canada’s economy is set to weaken amid ongoing trade wars even though the U.S. has stepped back from broad reciprocal tariffs and applied only targeted tariffs on Canada.

U.S. tariffs on China and other trading partners, along with growing uncertainty, is likely to slow U.S. growth meaningfully and weigh on Canadian growth. Lower oil prices won’t help as well.

Canada’s Five-Year Financial Markets Outlook—April 2025

Just as most central banks, including Canada’s, were set to declare victory over inflation, economic chaos emerging from the United States casts doubt on this, while presenting potentially unsolvable policy dilemmas. The Bank of Canada seeks to keep public inflation expectations near 2 per cent but has limited maneuverability, and Canadians and their leaders are scrambling to adjust policy on-the-fly.

Bank of Canada drops plans to issue digital currency

The Bank of Canada is ending its work on issuing a digital Canadian dollar four years after the central bank began studying the possibility.

On its website, the Bank of Canada announced Thursday it was “scaling down its work on a retail central bank digital currency.”

The bank explained the decision by saying its research work on the digital Canadian dollar was complete and other payments issues had become more pressing.

Canadians becoming more optimistic about their finances as Bank of Canada cuts rates

Canadians continue to show more green shoots of optimism regarding their financial prospects as the Bank of Canada cuts interest rates, suggests the most recent results of a survey that tracks how they feel about their money situation and the economy.

Is Canadian FinTech making a comeback?

The Nuvei and Plusgrade buyouts propelled investment in Canada’s FinTech sector to a record high in the first half of the year, according to a new KPMG report. Nuvei announced a whopping $6.3-billion USD exit from the public market in the second quarter, pushing overall investment in the sector to $7.8 billion USD. That surpasses the total deal value raised—$7 billion USD—during the entirety of 2021. Does that mean Canadian FinTech is back? Possibly. Let’s break it down.

Canada’s Banks are Standing by Canadians

To confront the financial dimensions of pandemic, Canada’s banking sector has worked in lockstep with the federal government, the Bank of Canada and regulators to immediately implement a series of relief initiatives, redeploying staff to create tailored support plans for individuals and small businesses to help manage financial uncertainty and help blunt the economic impact of COVID‑19.

Gap between Canada’s rich and poor widens at record pace on inflation, higher rates

Want to improve your credit score? Experts explain what you need to know—and do. Many people are at a loss when it comes to understanding how credit scores work. Yet that score can have a huge impact on any credit application they might make. Not only do financial institutions check credit scores; so do employers, landlords, insurance companies, and mobile serve providers. They all want to know who they are dealing with because the higher the score, the less risk they need to take on. Hence, the better the deal they can offer. Here are some credit score basics and tips on how to improve your score.

Expert advice on how to build a stronger credit score

Want to improve your credit score? Experts explain what you need to know—and do. Many people are at a loss when it comes to understanding how credit scores work. Yet that score can have a huge impact on any credit application they might make. Not only do financial institutions check credit scores; so do employers, landlords, insurance companies, and mobile serve providers. They all want to know who they are dealing with because the higher the score, the less risk they need to take on. Hence, the better the deal they can offer. Here are some credit score basics and tips on how to improve your score.

What is a recession? Here’s how a hit to Canada’s economy might impact you

Economists, market watchers, businesses and everyday Canadians are all asking the same question lately as inflation and interest rates take a bite out of household finances: are we headed for a recession? A majority of business owners and consumers are saying yes, according to surveys released this week from the Bank of Canada that show most respondents are reining in their spending ahead of a possible downturn.

Bank of Canada surveys show how Canadians are gearing up for a possible recession

Businesses and consumers alike are trimming their spending plans as higher interest rates bite and a possible recession looms, according to new surveys from the Bank of Canada.The central bank’s fourth-quarter surveys of business and consumer sentiments, published Monday, showed an overall dour outlook for 2023, with the majority of both polled cohorts indicating they expect a recession in the next 12 months.

Consumers can now get charged for using credit cards in Canada. What does this mean?

Credit card companies have always passed on fees, known as interchange fees, to merchants. As part of a class-action settlement earlier this year, merchants now have the option of passing that fee on to consumers who use credit cards. Ashworth spoke about what this transparency means, about the business of credit cards, the lack of competition and more. As always the interview is edited for clarity and brevity.

Investors more selective on Canadian fintech ‘reset’

Last year was record-breaking for investment in the Canadian fintech sector, but things have cooled significantly. After US$1.9 billion in investment during the second half of 2021, the first six months of 2022 saw just $810 million from 85 deals. That was well below the year-ago figure of $5.4 billion from 108 deals, although H1 2021 did include one of the strongest quarters on record. “The market downturn and ensuing lower tech valuations caused investors to hit the ‘pause button’ over the last few months, but with so much investment flowing into fintech last year, we see it as a re-balancing of expectations, or a sector reset if you will,” says Geoff Rush, National Industry Leader for Financial Services at KPMG in Canada.

How Fintech Can Deliver on Its Social Impact Promises

The financial technology (fintech) industry seems to strike investors’ goldilocks dream of doing exceptionally well while creating exceptional good. Based on the promise of positive social impact through financial inclusion, fintech has seen meteoric growth while also capturing more impact-related investment funds than any other industry. In the last year alone, equity funding raised by fintech companies around the world nearly doubled. To date, fintech companies have a collective global market value of $5 trillion and industry growth is expected to be above 23% for the next five years.

Canadian FinTech Continues To Heat Up After A Strong Year In 2021

The second half of 2021 in FinTech continued to see record funding with a total of 77 venture capital-backed deals over 72 companies for a total of $1.7 billion in disclosed funding. This includes all rounds of venture capital-based financing, angel investments and accelerator and incubator investments across FinTech in Canada. When compared to the first half of 2021, we did see a slight drop in financing rounds due to slower periods in October and November of 2021. Despite this, however, 2021 proved to be a record year for FinTech investment in Canada.

Canada’s Hottest FinTech Lending Trends for 2022 Revealed in Latest Research

According to Smarter Loans’ Canada FinTech Lending Study 2022, which gathered the feedback of 2,462 Canadian fintech lending customers, the demand for digitally accessible financial products in Canada continues to grow at a fast pace.

Technology-led innovation in banking

Technology is changing the way financial products and services are accessed and used by Canadians. The innovative financial technologies (FinTech) being introduced by banks and FinTech businesses in Canada are increasing choice and improving convenience for customers.

The pandemic is inspiring Gen Z to build financial resilience

The coronavirus pandemic has tested the limits of Canadians over the past 20 months. What began as a health crisis quickly morphed into an economic crisis, with the spread of COVID-19 shocking large segments of the economy and leaving many without paycheques. While no generation has been unaffected by this disruptive event, the financial impact was distributed unevenly.